The global smartphone market is undergoing a structural shift as rising component costs and geopolitical uncertainty push leading manufacturers to move away from low-cost, high-volume strategies and prioritize premium, high-value portfolios, reports Omdia.

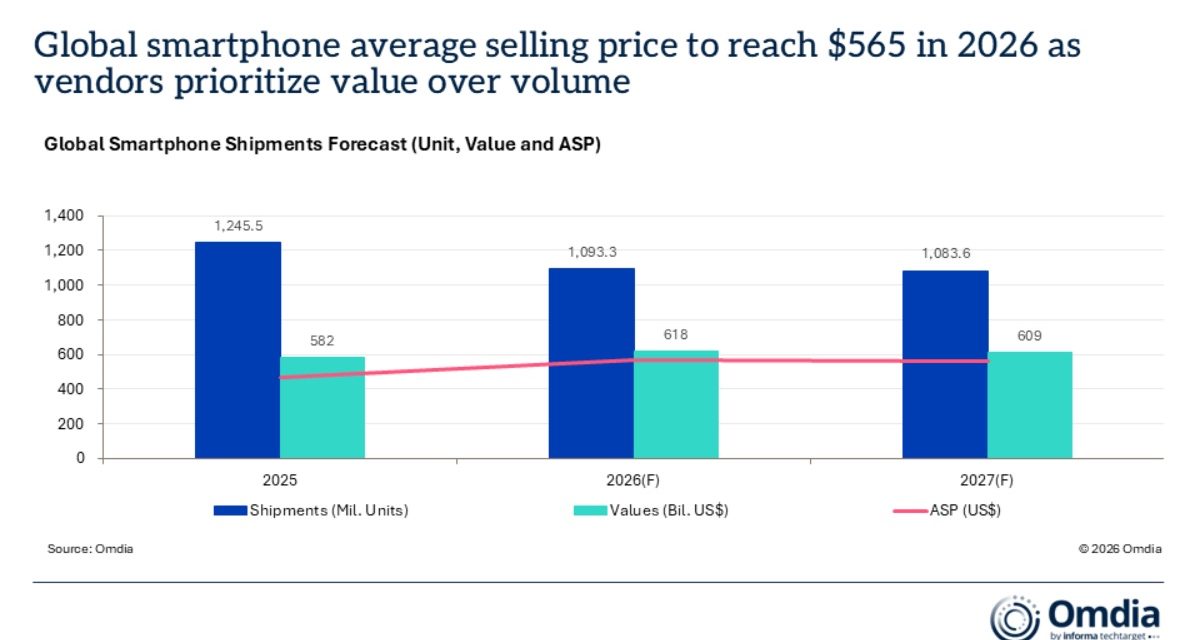

According to the research’s global smartphone forecast, total global smartphone shipments are forecast to contract by 12.2% year-on-year (YoY) in 2026, dropping to 1,093 million units. This represents a decline of 152 million units compared with 2025. Despite this shipment contraction, total market value is projected to grow by 6.1% YoY over the same period.

When it comes to Apple, Due to explosive AI industry demand for DRAM and NAND memory, CEO Tim Cook has confirmed that consumer device price increases are unavoidable, with estimates ranging from a $100 bump on Pro models up to a 15% overall increase for smartphones.

A historic surge in average selling prices

This divergence between shipment volume and market value is being fueled by a sharp rise in retail pricing, per Omdia. The global smartphone average selling price (ASP) is forecast to increase from $467 in 2025 to $565 in 2026. This 21% jump – equivalent to $98 – marks an all-time high in both growth rate and dollar value for the industry.

This pricing surge reflects severe margin pressures across the supply chain. Average DRAM and NAND flash memory prices rose by more than 80% quarter-on-quarter in 1Q26, with further increases already seen in 2Q26. While memory price hikes are expected to slow to single-digit growth rates in the second half of the year, component costs will remain structurally elevated, forcing vendors to pass some of these costs onto consumers.

“The smartphone industry is currently going through a period of significant disruption, as vendors work to manage short-term component cost pressures as effectively as possible,” says Jusy Hong, Senior Research Manager at Omdia. “Some vendors are gaining early-mover advantages by increasing component inventories to minimize the impact of future price hikes. Once the DRAM and NAND pricing starts to stabilize and plateau at a new level, the market is expected to enter a phase of stabilization, where the focus will shift back to other strategic priorities. This transition is expected towards the second half of 2027.”

Many industry players will be waiting for the readjustment phase, when component prices start to move downwards, he adds. At this stage, vendors with leaner structures will be better positioned to benefit from price declines, and excess inventory could become a major hurdle.

“The transition to a readjustment phase is currently anticipated in early 2028, driven by expected increases in supply capacity. Short-term ease could arrive earlier, depending on how AI datacenter demand develops,” Hong says.

Strategic Pivot and Regional Impact

To protect margin, global vendors are actively scaling back their low-end product lines and increasing production shares for mid-to-high-end smartphones in their portfolios. Omdia says this strategic pivot will impact regions differently:

- Emerging Markets: Demand is expected to fall heavily in Africa, the Middle East, and Latin America. These regions rely heavily on low-end devices and are highly sensitive to price increases.

- Developed Markets: Premium-heavy developed markets are expected to be more resilient, with milder shipment declines.

- Vendor Portfolios: Almost every major smartphone brand— apart from Apple—has raised retail prices for new-generation products to offset higher manufacturing costs.

“Vendors are also increasingly relying on wider business models and portfolios to strengthen operational resilience,” says said Runar Bjorhovde, Omdia Principal Analyst for smartphones. “ Vendors and regions with a high dependence on budget smartphones as their primary customer engagement will be particularly exposed. The strongest position will be held by vendors that can capture additional high-value and high-margin streams from each user.”

He adds that this will typically include cross-selling other ecosystem devices, upselling services and subscriptions that increase the lifetime user value, and expanding opportunities to monetize the installed base,

Long-Term Outlook and Delayed Recovery

Omdia forecasts that the global smartphone market contraction will extend into 2027, although the shipment decline is forecast to slow significantly to 0.9%. Even as memory prices are projected to begin correcting in 2027, the baseline cost of manufacturing sub-$100 smartphones is expected to remain too high to support significant decreases in end-user pricing.

Meaningful volume recovery for the industry is therefore expected to begin in 2028, according to Omdia Looking ahead, top global smartphone vendors are expected to remain highly conservative about expanding entry-level lineups, adds the research group. The ultra-low-end smartphone segment is projected to shift away from major global brands and towards smaller, local and regional manufacturers.

I hope you’ll help support Apple World Today by becoming a patron. Almost all our income is from Patreon support and sponsored posts. Patreon pricing ranges from $2 to $10 a month. Thanks in advance for your support.

Article provided with permission from AppleWorld.Today