Amid ongoing memory and supply chain disruptions, IDC has made significant downward revisions to its PC and tablet outlook.

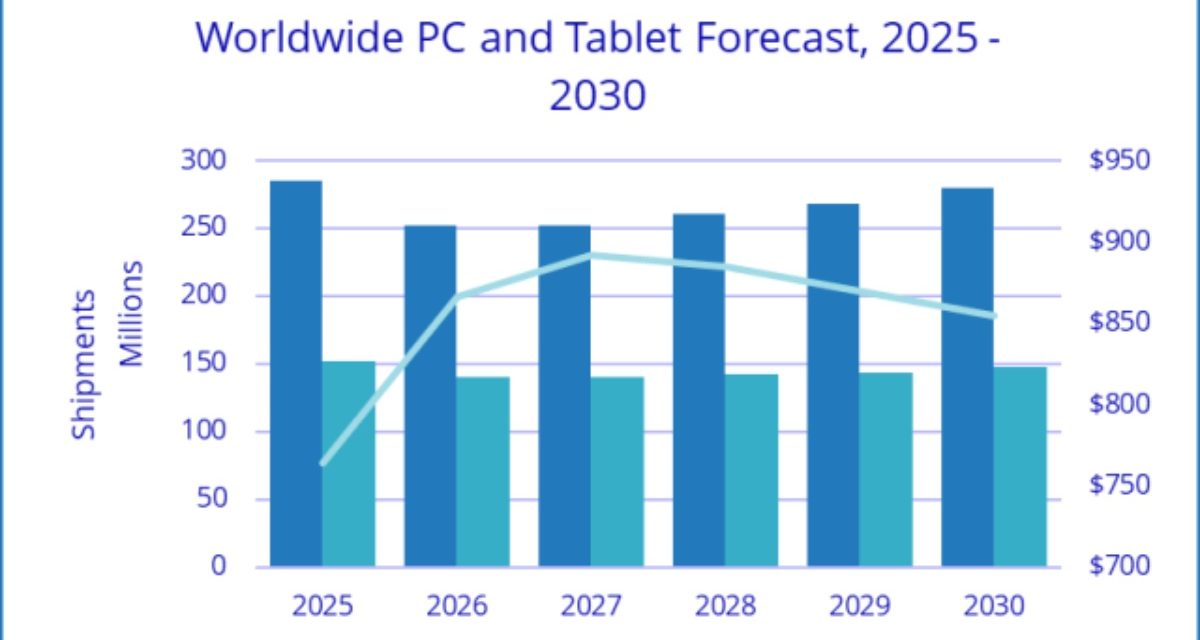

According to the latest data from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker, global PC shipments are now expected to decline 11.3% in 2026 —a substantial reduction from the -2.4% outlook published in November 2025. Tablet shipments are similarly forecast to fall 7.6% this year.

The research group says these reductions are driven by a convergence of memory shortages, rising component prices, and broader supply constraints, all of which are expected to limit production well into 2027, making recovery timing a challenging and shifting target. It is also worth noting that at the time this forecast was published, the conflict in the Middle East had not yet escalated to its current level, adding yet another significant challenge for many industries, including technology and hardware, according to Ryan Reith, group vice president, Devices and Consumer, IDC.

“The overall tech industry, as well as many others, continues to face uncontrollable headwinds that, when compounded, result in massive disruption,” he added. “The lists of industry and geopolitical events that continue to grow is making decision‑making—and even survival in some sectors—nearly impossible. What has turned all of this from a million‑dollar question into a trillion‑dollar question is the complete uncertainty around when these pressures will subside.”

Even in the shadow of these shortages, the market retains pockets of resilience, Reith said. Higher average selling prices (ASPs) are expected to lift total market value, with PCs growing 1.6% to $274 billion and tablets expanding 3.9% to $66.8 billion in 2026.

“The era of bargain-priced PCs and tablets is behind us for now, as rising ASPs and component costs shift the market’s balance of power,” said Jitesh Ubrani, research manager for IDC’s Worldwide Mobile Device Trackers. “Memory shortages will persist well into 2027. While we anticipate some easing of prices beginning in 2028, the market is unlikely to return to the pricing levels seen in 2025. Instead, we expect a new normal defined by structurally higher ASPs and a corresponding softening in long-term demand.”

Looking ahead, IDC anticipates vendors prioritizing supply chain resilience, more flexible component sourcing strategies, and explore down-spec’ing options to control costs while offering more affordable devices. These dynamics will play a notable role in defining end user adoption in the coming years.

I hope you’ll help support Apple World Today by becoming a patron. Almost all our income is from Patreon support and sponsored posts. Patreon pricing ranges from $2 to $10 a month. Thanks in advance for your support.

Article provided with permission from AppleWorld.Today