As U.S. credit card spending continues to set records in the face of an uncertain economy and growing competition from alternative lenders and digital payment apps, credit card issuers are in a pitched battle to win new customers with ever-richer rewards and incentive programs.

According to the J.D. Power 2019 Credit Card Satisfaction Study,SM released today, the credit card incentive war may have reached its peak, with no real change in customers saying they fully understand the rewards and ancillary benefits available to them.

“The average credit card customer today has roughly 16 different benefits available, yet only about one-third of customers say they completely understand all of the benefits available to them,” says John Cabell, director, Wealth and Lending Intelligence at J.D. Power. “While the last several years of rewards-based competition among issuers has served to steadily increase overall customer satisfaction, issuers may have wrung all of the value they can out of this approach. They should now turn their attention to communication to help customers extract the full value from their products and buttress themselves against competition from a growing crop of rivals.”

Following are some key findings of the 2019 study:

° Complex offerings only valued with customer understanding: Facing a rich mix of rewards and benefits, 66% of consumers completely understand rewards offerings but just 36% fully understand their supplementary benefits. Credit card customers who say they fully understand the benefits available to them have satisfaction scores that are 165 points higher than those who do not completely understand their benefits offerings (864 vs. 699 on a 1,000-point scale). Also, customers who completely understand their benefits cite significantly fewer benefits available than those who do not understand their benefits.

° Customer-focused communication around card benefits lacking: Benefits and services is tied with credit card terms as the lowest-rated factor in the study (758), with customers having the lowest levels of satisfaction with the issuer’s explanation of card benefits. Among the most problematic individual benefits that either caused confusion or did not function as expected, most are travel-related, such as free late checkout and free companion ticket.

° Room for reputational improvement: On a 7-point brand image scale, customers give credit card issuers a score of 4.97 on being customer-driven vs. profit-driven, and 41% say they “strongly agree” that their issuer acts in their best interest. As branded products like the Apple Card enter the market, issuers should communicate clearly and deliver consistently on customer promises to boost their image.

° Cyber security and identity theft fears decline in 2019: Recent, high profile data breaches have not yet had a negative effect on customer perception of security, with 52% of customers reporting that they “strongly agree” that their credit card issuer protects their personal identity, up from 49% in 2018. However, given the timing of events, monitoring fluctuations in customer trust in the coming months will be important.

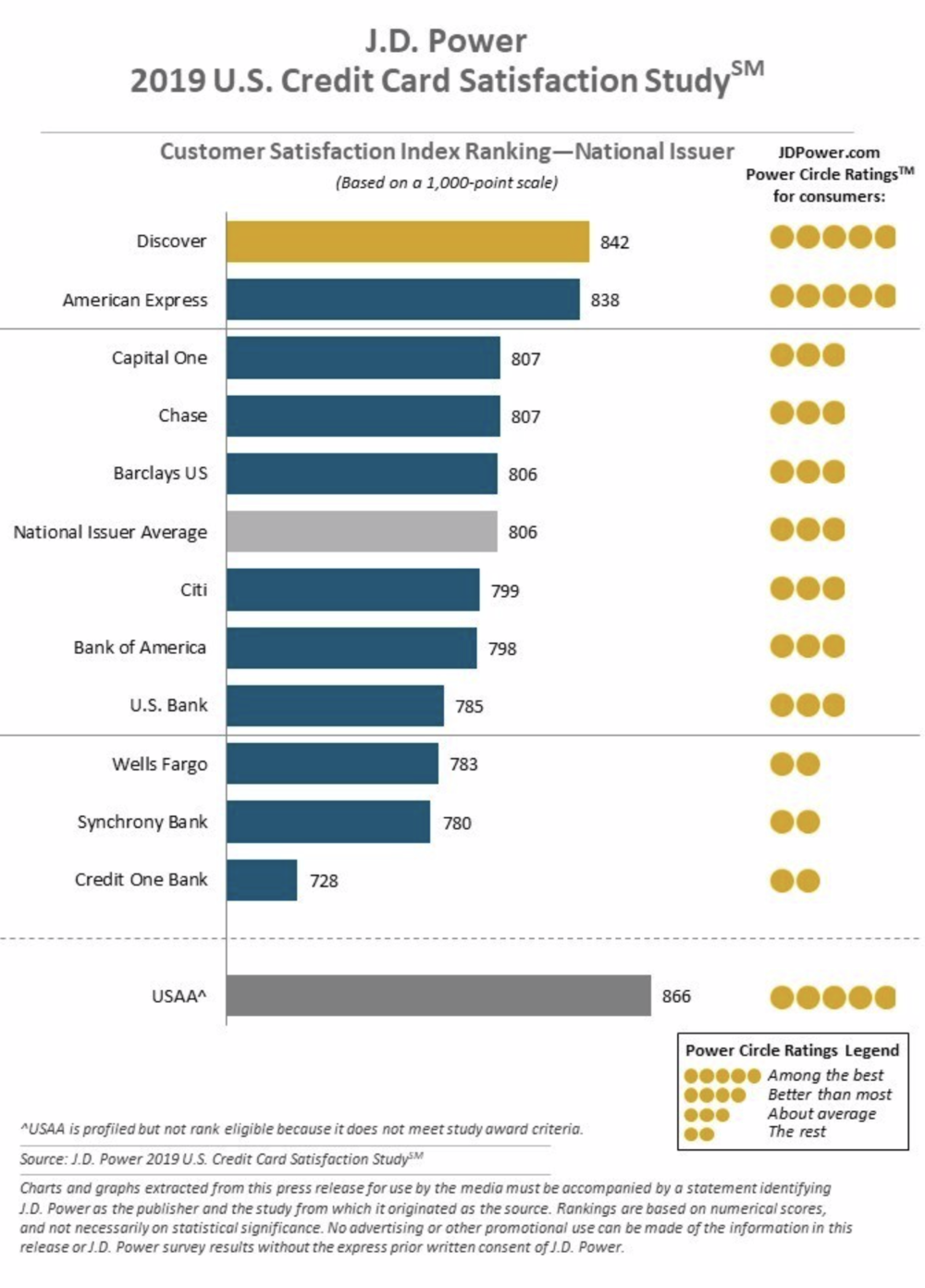

Discover ranks highest in customer satisfaction among national issuers, with a score of 842. American Express (838) ranks second, while and Capital One and Chase (807 each) rank third in a tie.

A new segment for regional bank issuers has been created and the inaugural award winner is BB&T, with a score of 811. PNC (810) ranks second.

The U.S. Credit Card Satisfaction Study, now in its 13th year, measures customer satisfaction with credit card issuers by examining six factors (in descending order of importance): interaction; credit card terms; communication; benefits and services; rewards; and key moments. The study includes responses from 28,236 credit card customers and was fielded from September 2018 through June 2019.

For more information about the 2019 U.S. Credit Card Satisfaction Study, visit https://www.jdpower.com/business/resource/us-credit-card-satisfaction-study.