Worldwide spending on public cloud services and infrastructure is forecast to reach $210 billion in 2019, an increase of 23.8% over 2018, according to the latest update to the International Data Corporation (IDC) Worldwide Semiannual Public Cloud Services Spending Guide.

Although annual spending growth is expected to slow slightly over the 2017-2022 forecast period, the market is forecast to achieve a five-year compound annual growth rate (CAGR) of 22.5% with public cloud services spending reaching $370 billion in 2022.

“Most organizations have adopted the public cloud as a cost-effective platform for hosting enterprise applications and for developing and deploying customer-facing solutions,” said Eileen Smith, program director, Customer Insights and Analysis. “Over the next five years, IDC believes that cloud platforms and ecosystems will serve as the launchpad for an explosion in the scale and pace of digital innovation. The result will be ‘multiplied innovation’ with as many new applications deployed in the cloud as prior generations deployed over the previous four decades.”

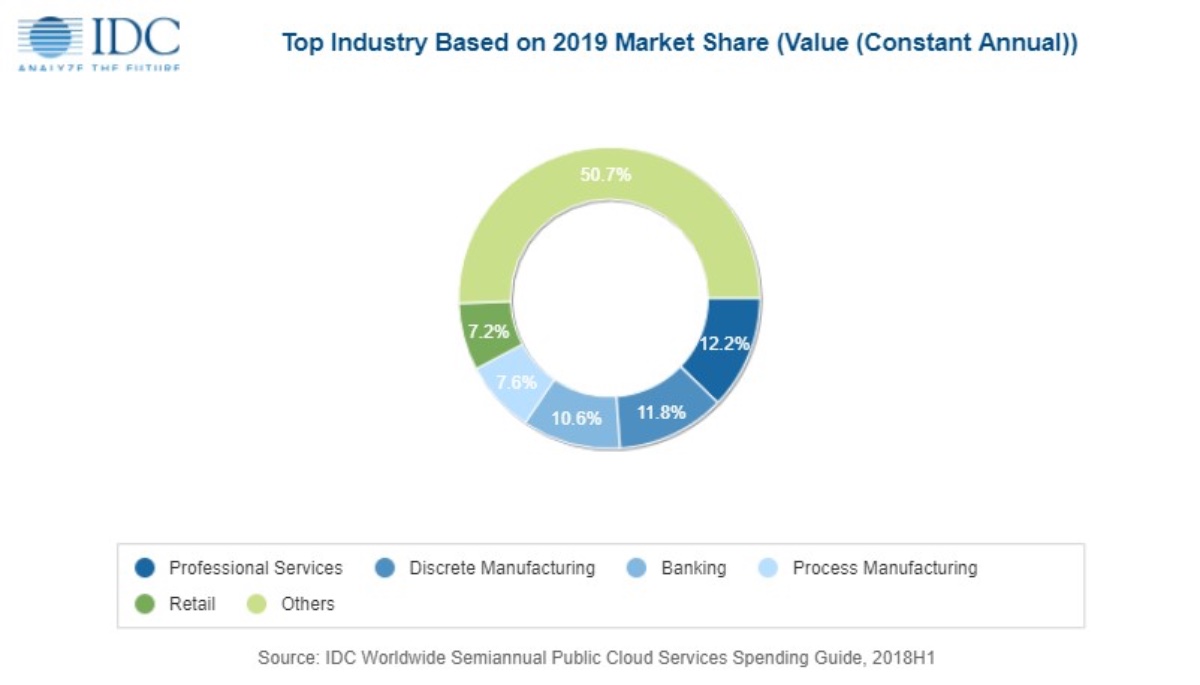

Three industries – professional services, discrete manufacturing, and banking – will each spend more than $20 billion on public cloud services this year, accounting for more than one third of the worldwide total. The process manufacturing and retail industries will round out the top five with spending of more than $15 billion each.

These will remain the top five industries in 2022 due to their continued investment in public cloud solutions. The industries that will see the fastest spending growth over the five-year forecast period are professional services (26.4% CAGR), retail (24.0% CAGR), and personal and consumer services (24.0% CAGR).

Software as a Service (SaaS) will be the largest category of cloud computing, capturing more than half of all public cloud spending in 2019. SaaS spending, which is comprised of applications and system infrastructure software (SIS), will be dominated by applications purchases. The leading SaaS applications will be enterprise resource management (ERM) and customer relationship management (CRM), followed by content workflow and management applications and collaborative applications.

Infrastructure as a Service (IaaS) will be the second largest category of public cloud spending in 2019, followed by Platform as a Service (PaaS). IaaS spending, comprised of servers and storage devices, will be the fastest growing category of cloud spending with a five-year CAGR of 33.7%. PaaS spending will be the second-fastest growing category (29.8% CAGR) led by purchases of data management software application platforms, integration and orchestration middleware, and data access, analysis and delivery applications.

The United States will be the largest geographic public cloud market with spending forecast to be $124.6 billion in 2019. China will be the second largest market at $10.5 billion, followed closely by the United Kingdom ($10.0 billion) and Germany ($9.5 billion).

Japan will round out the top five with $7.4 billion in public cloud spending this year. China will experience the fastest growth in public cloud services spending over the five-year forecast period (44.9% CAGR). Latin America will also deliver strong public cloud spending growth, led by Brazil (38.8% CAGR), Colombia (38.5% CAGR) and Argentina (38.4% CAGR).

Very large businesses (more than 1000 employees) will account for more than half of all public cloud spending this year, while medium-size businesses (100-499 employees) will deliver another 20% of the worldwide total. Small businesses (10-99 employees) will edge out large businesses (500-999 employees) for the third position. With the exception of the very large business category, all the other company size categories, including small office (1-9 employees) will experience public cloud spending growth greater than the 22.5% CAGR of the overall market.