Worldwide spending on the technologies and services that enable the digital transformation (DX) of business practices, products, and organizations is forecast to reach $1.97 trillion in 2022, according to a new update to the International Data Corporation (IDC) Worldwide Semiannual Digital Transformation Spending Guide.

DX spending is expected to steadily expand throughout the 2017-2022 forecast period, achieving a five-year compound annual growth rate of 16.7%.

“IDC predicts that, by 2020, 30% of G2000 companies will have allocated capital budget equal to at least 10% of revenue to fuel their digital strategies,” says Shawn Fitzgerald, research director, Worldwide Digital Transformation Strategies. “This shift toward capital funding is an important one as business executives come to recognize digital transformation as a long-term investment. This commitment to funding DX will continue to drive spending well into the next decade.”

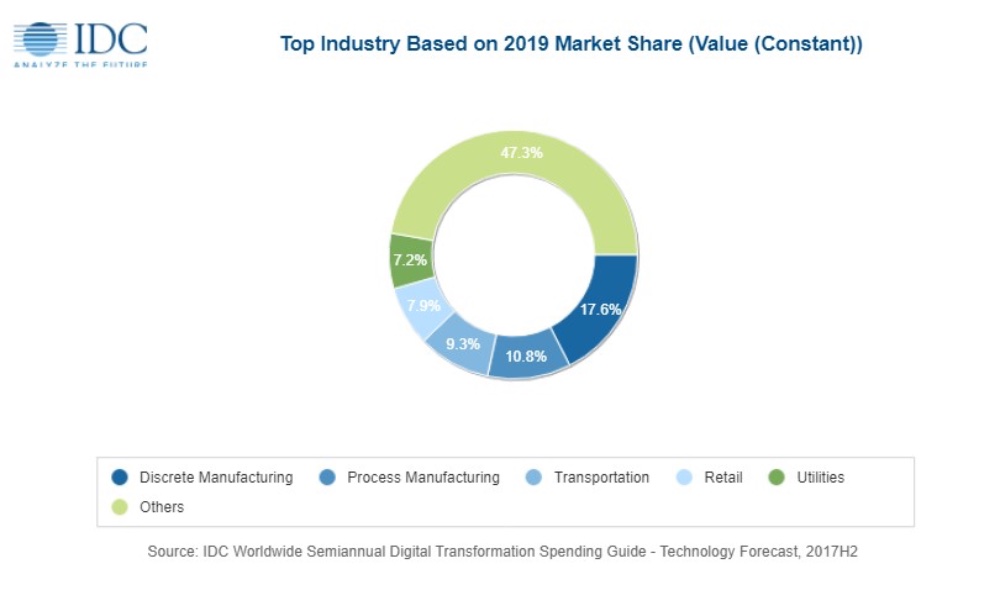

Four industries will be responsible for nearly half of the $1.25 trillion in worldwide DX spending in 2019: discrete manufacturing ($220 billion), process manufacturing ($135 billion), transportation ($116 billion), and retail ($98 billion). For the discrete and process manufacturing industries, the top DX spending priority is smart manufacturing.

IDC expects the two industries to invest more than $167 billion in smart manufacturing next year along with significant investments in digital innovation ($46 billion) and digital supply chain optimization ($29 billion). In the transportation industry, the leading strategic priority is digital supply chain optimization, which translates to nearly $65 billion in spending for freight management and intelligent scheduling.

Meanwhile, the top priority for the retail industry is omni-channel commerce, which will drive investments of more than $27 billion in omni-channel commerce platforms, augmented virtual experience, in-store contextualized marketing, and next-generation payments.

The DX use cases – discretely funded efforts that support a program objective – that will see the largest investment across all industries in 2019 will be freight management ($60 billion), autonomic operations ($54 billion), robotic manufacturing ($46 billion), and intelligent and predictive grid management for electricity, gas, and water ($45 billion). Other use cases that will see investments in excess of $20 billion in 2019 include root cause, self-healing assets and automated maintenance, and quality and compliance.

“Industry spending on DX technologies is being driven by core innovation accelerator technologies with IoT and cognitive computing leading the race in terms of overall spend,” says Eileen Smith, program director with IDC’s Customer Insights and Analysis Group. “The introduction of IoT sensors and communications capabilities is rapidly transforming manufacturing processes as well as asset and inventory management across a wide range of industries. Similarly, artificial intelligence and machine learning are dramatically changing the way businesses interact with data and enabling fundamental changes in business processes.”

From a technology perspective, hardware and services spending will account for more than 75% of all DX spending in 2019. Services spending will be led by IT services ($152 billion) and connectivity services ($147 billion) while business services will experience the fastest growth (29.0% CAGR) over the five-year forecast period.

Hardware spending will be spread across a number of categories, including enterprise hardware, personal devices, and IaaS infrastructure. DX-related software spending will total $288 billion in 2019 and will be the fastest growing technology category with a CAGR of 18.8%.

The U.S. and China will be the two largest geographic markets for DX spending, delivering more than half the worldwide total in 2019. In the U.S., the leading industries will be discrete manufacturing ($63 billion), transportation ($40 billion), and professional services ($37 billion) with DX spending focused on IT services, applications, and connectivity services.

In China, the industries spending the most on DX will be discrete manufacturing ($60 billion), process manufacturing ($35 billion), and utilities ($27 billion). Connectivity services and enterprise hardware will be the largest technology categories in China.