Worldwide spending on security-related hardware, software, and services is forecast to reach $133.7 billion in 2022, according to a new update to the Worldwide Semiannual Security Spending Guide from International Data Corporation (IDC).

Although spending growth is expected to gradually slow over the 2017-2022 forecast period, the market will still deliver a compound annual growth rate (CAGR) of 9.9%. As a result, security spending in 2022 will be 45% greater than the $92.1 billion forecast for 2018, the research group predicts.

“Privacy has grabbed the attention of Boards of Directors as regions look to implement privacy regulation and compliance standards similar to GDPR. Frankly, privacy is the new buzz word and the potential impact is very real. The result is that demand to comply with such standards will continue to buoy security spending for the foreseeable future,” says Frank Dickson, research vice president, Security Products.

IDC forecasts that security-related services will be both the largest ($40.2 billion in 2018) and the fastest growing (11.9% CAGR) category of worldwide security spending. Managed security services will be the largest segment within the services category, delivering nearly 50% of the category total in 2022. Integration services and consulting services will be responsible for most of the remainder.

Security software is the second-largest category with spending expected to total $34.4 billion in 2018. Endpoint security software will be the largest software segment throughout the forecast period, followed by identity and access management software and security and vulnerability management software.

IDC says the latter will be the fastest growing software segment with a CAGR of 10.7%. Hardware spending will be led by unified threat management solutions, followed by firewall and content management.

Banking will be the industry making the largest investment in security solutions, growing from $10.5 billion in 2018 to $16.0 billion in 2022. Security-related services, led by managed security services, will account for more than half of the industry’s spend throughout the forecast.

IDC says the second and third largest industries, discrete manufacturing and federal/central government ($8.9 billion and $7.8 billion in 2018, respectively), will follow a similar pattern with services representing roughly half of each industry’s total spending. The industries that will see the fastest growth in security spending will be telecommunications (13.1% CAGR), state/local government (12.3% CAGR), and the resource industry (11.8% CAGR).

“Security remains an investment priority in every industry as companies seek to protect themselves from large scale cyber attacks and to meet expanding regulatory requirements,” says Eileen Smith, program director of IDC’s Customer Insights and Analysis. “While security services are an important part of this investment strategy, companies are also investing in the infrastructure and applications needed to meet the challenges of a steadily evolving threat environment.”

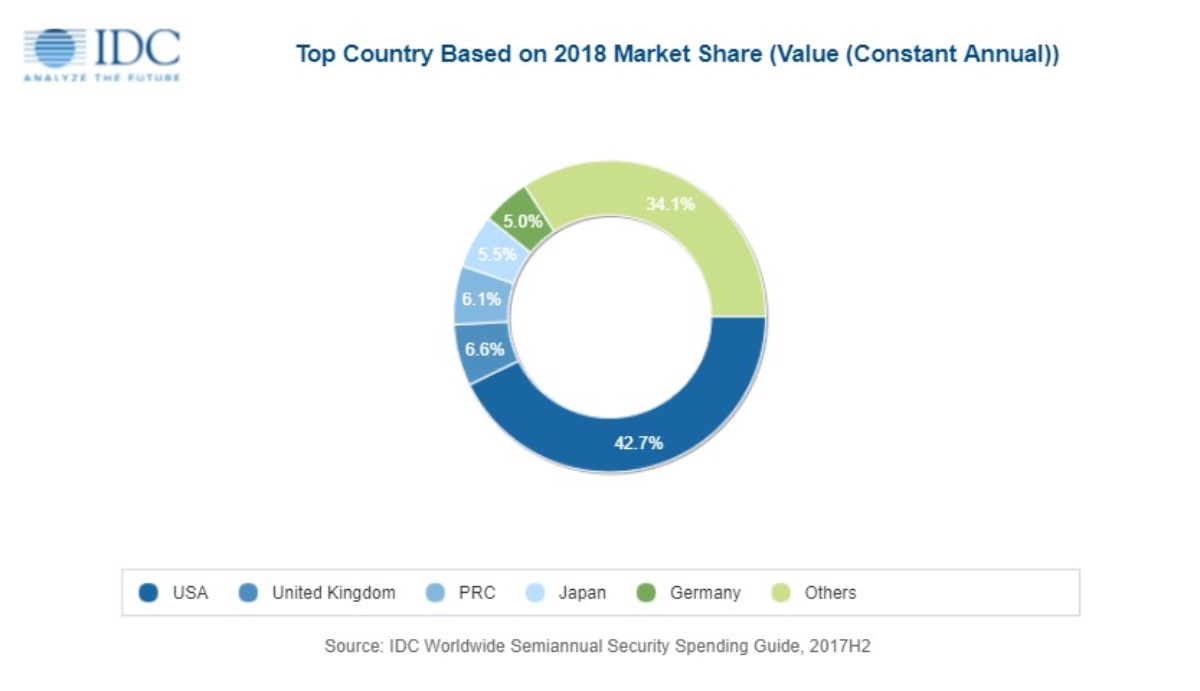

The United States will be largest geographic market for security solutions with total spending of $39.3 billion this year. The United Kingdom will be the second largest geographic market in 2018 at $6.1 billion followed by China ($5.6 billion), Japan ($5.1 billion), and Germany ($4.6 billion). The leading industries for security spending in the U.S. will be discrete manufacturing and the federal/central government.

In the UK, banking and discrete manufacturing will deliver the largest security spending while telecommunications and banking will be the leading industries in China. China will see the strongest spending growth with a five-year CAGR of 26.6%. Malaysia and Singapore will be the second and third fastest growing regions with CAGRs of 21.1% and 18.2%, respectively.

From a company size perspective, large and very large businesses (those with more than 500 employees) will be responsible for nearly two thirds of all security-related spending in 2018. Large (500-999 employees) and medium businesses (100-499 employees) will see the strongest spending growth over the forecast, with CAGRs of 11.8% and 10.0% respectively.

However, IDC says very large businesses (more than 1,000 employees) will grow nearly as fast with a five-year CAGR of 10.1%. Small businesses (10-99 employees) will also experience solid growth (8.9% CAGR) with spending expected to be more than $8.0 billion in 2018.